Home Ownership Dream is Slipping Away from Younger Australians

The ongoing housing crisis remains a hot topic and one of the major concerns for many Australians. Figures from Equifax1 confirm a troubling trend: home ownership in Australia becomes a progressively distant aim for younger people.

The ongoing housing crisis remains a hot topic and one of the major concerns for many Australians. Figures from Equifax1 confirm a troubling trend: home ownership in Australia becomes a progressively distant aim for younger people.

Two years ago, the trajectory of interest rates in Australia took a noticeable turn, starting a steady climb and ending a prolonged period of low-rate environment. This shift has sparked a broad debate regarding its potential impact on the Australian residential property market, housing affordability and overall financial implications for households. We note that higher interest rates were widely anticipated to put downward pressure on property prices via lower borrowing power of aspiring homeowners and increased incidence of distressed sales among existing mortgagors. However, these effects have been more than offset by increased demand from record high immigration along with a substantial undersupply of new housing that now comes at an elevated cost, which has made it much harder for many Australians to afford buying a home.

Over the past two years, the average cost of house construction in Australia increased by 17.5%2. Similarly, median property prices increased across Australia and in some regions (mainly QLD, SA and WA) surged by 10.0% - 30.0% between March 2022 and March 20243. At the same time, the increase in variable interest rates on new mortgages from 2.6% to 6.3% over this period reduced the average borrowing power of many Australians by more than 35.0% (ignoring the effects of real wage decline). As a result of this widening gap between the amount they need to secure their own home and their maximum borrowing capacity, many Australians have been priced out of the market, delaying their home purchasing and continuing to pay record high rental prices.

Expectedly, these affordability challenges are not equally experienced by different social groups. As suggested by the decreasing share of new housing loans from lower-income borrowers in Australia (the high loan-to-income ratio group), they have been increasingly excluded from the new mortgages market (refer to the graph below)4. Additionally, data collected by Equifax indicate that it is younger Australians who face disproportionately bigger hurdles on their journey to home ownership, compared to their older peers.

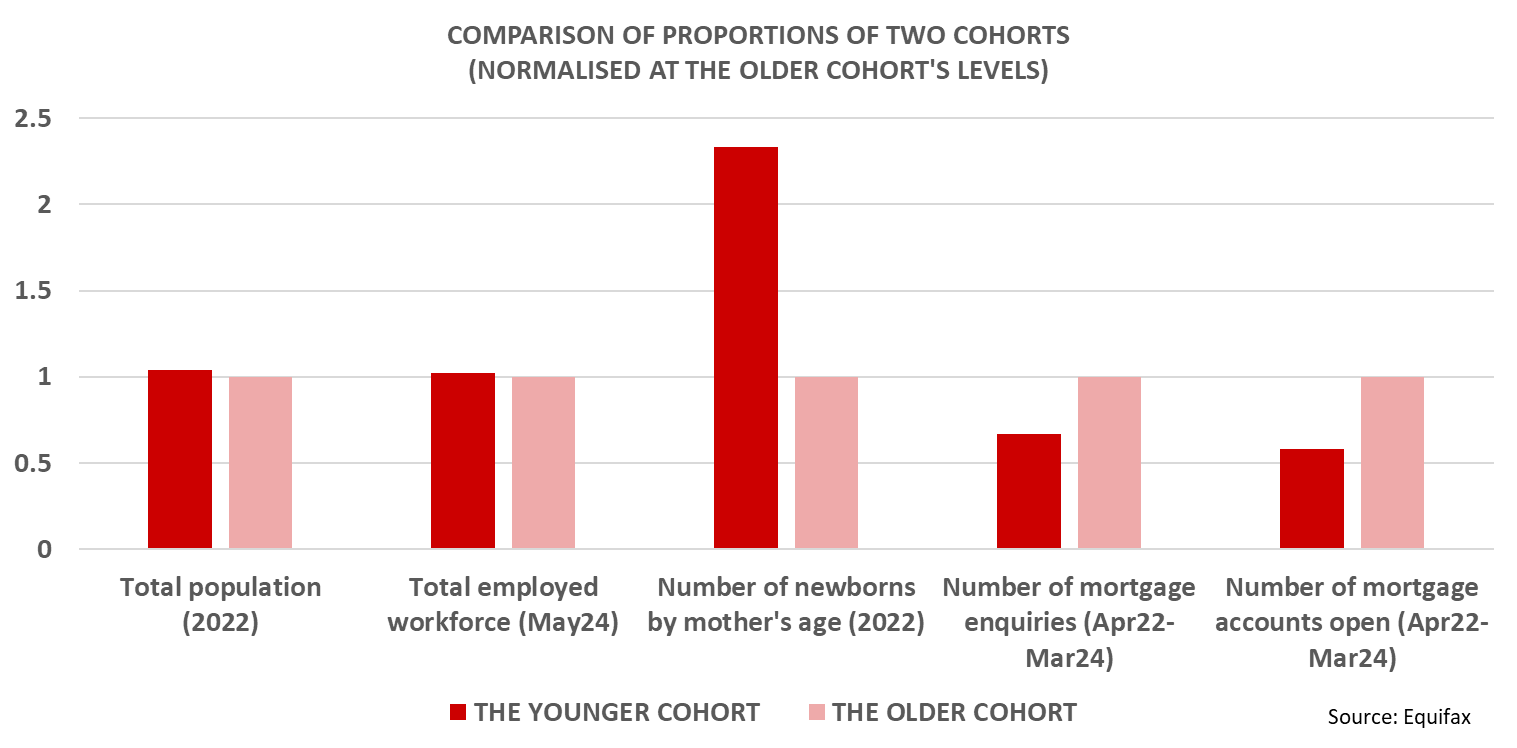

The age groups of our particular interest were 25-34 years old (‘the younger cohort’) and 35-44 years old (‘the older cohort’), who account for 14.4% and 13.8% of the Australian population, respectively5. We further note that these two age groups are also almost equally represented in the workforce, constituting 23.7% and 22.7% of employed Australians, respectively6. Finally, women of the younger cohort gave birth to 61.9% of Australian babies in 2022, compared to 26.5% delivered by the older cohort women7.

Surprisingly, mortgage data collected by Equifax over the past two years indicate that the younger cohort that delivers the greater proportion of babies and most in need of housing, is underrepresented when it comes to getting a home loan, compared to the older cohort. Between 01 April 2022 and 01 April 2024, there were 49.8% more reported mortgage requests made by the older cohort than by the younger cohort. The number of new mortgage accounts opened by the older cohort over the same period was 72.0% higher compared to the younger cohort. Finally, the proportion of open accounts out of applications received is materially and consistently lower for the younger cohort and has considerably reduced over the past two years8.

While there are several plausible explanations for this evident disproportion – earlier stages of career and mobile lifestyle are generally associated with lower income levels and saving bases, impacting their ability to meet the increased funding necessary to cover the surge in house prices - the core issue is insufficient financial capacity of young Australians. This hinders their access to the basic necessity of home ownership.

We note that various studies indicate a strong impact of housing market conditions on family formation, fertility rates, mental wellbeing and social justice. For example, Kadir Atalay et al. concluded in 2021 that housing price growth in Australia deters childbirth among renters9, while data collected in China indicate that rising housing prices can also delay the age of first marriage10. This issue is particularly acute, considering Australia’s steadily declining fertility rate and increasing reliance on immigrants. In 2020, Baker et al. found that prolonged housing affordability stress negatively impacts mental health11, whereas 2019 research found that citizens of Hong Kong experiencing housing affordability issues are likely to be less physically active, non-married and less educated.

While housing affordability might seem like personal issues of less fortunate younger Australians, it is likely to have long-term detrimental social-economic effects on Australian society. Apart from direct pressure on the government services associated with homelessness, physical and mental health systems, it also has a potential to impact the demographic and political profiles of Australia for the coming decades.

-Ends-

Reference list:

1 Equifax Australia Information Services & Solutions Pty Limited

2 ABS (Output of the Construction industries, subdivision and class index numbers)

3 ABS (Median Price and Number of Transfers)

4 APRA (Quarterly authorised deposit-taking institution statistics)

5 ABS (Regional population by age and sex, 2022)

6 ABS (Labour force status and Gross changes (flows) by Age, Sex, State and Territory)

7 ABS (Births, Australia, 2022)

8 Equifax’s proprietary data

9 Kadir Atalay, Ang Li, Stephen Whelan, Housing wealth, fertility intentions and fertility, Journal of Housing Economics, Volume 54, 2021, 101787, ISSN 1051-1377, https://doi.org/10.1016/j.jhe.2021.101787.

10 Chunkai Zhao, Boou Chen, Xing Li, Rising housing prices and marriage delays in China: Evidence from the urban land transaction policy, Cities, Volume 135,2023, 104214, ISSN 0264-2751,

https://doi.org/10.1016/j.cities.2023.104214.

11 Baker, E., Lester, L., Mason, K. et al. Mental health and prolonged exposure to unaffordable housing: a longitudinal analysis. Soc Psychiatry Psychiatr Epidemiol 55, 715–721 (2020). https://doi.org/10.1007/s00127-020-01849-1

Related Posts

Highlights:

Mitigate the surge in AI-generated digital forgeries by moving from document-based checks to source-verified payroll data Combat sophisticated salary staging and liar loans with an automated, single source of truth Establish digital trust at the point of contact to protect your organisation from credit and compliance risks.