Diverging Trends: Commercial and Residential vacancies at two opposite extremes

In a tale of two markets, Australia finds itself contending with starkly opposing realities in its real estate landscape. While the residential sector grapples with a severe shortage, commercial properties, particularly office spaces, are experiencing very high vacancies.

By Anuj Kindra, Chief Rating Analyst for Equifax Ratings

In a tale of two markets, Australia finds itself contending with starkly opposing realities in its real estate landscape. While the residential sector grapples with a severe shortage, commercial properties, particularly office spaces, are experiencing very high vacancies.

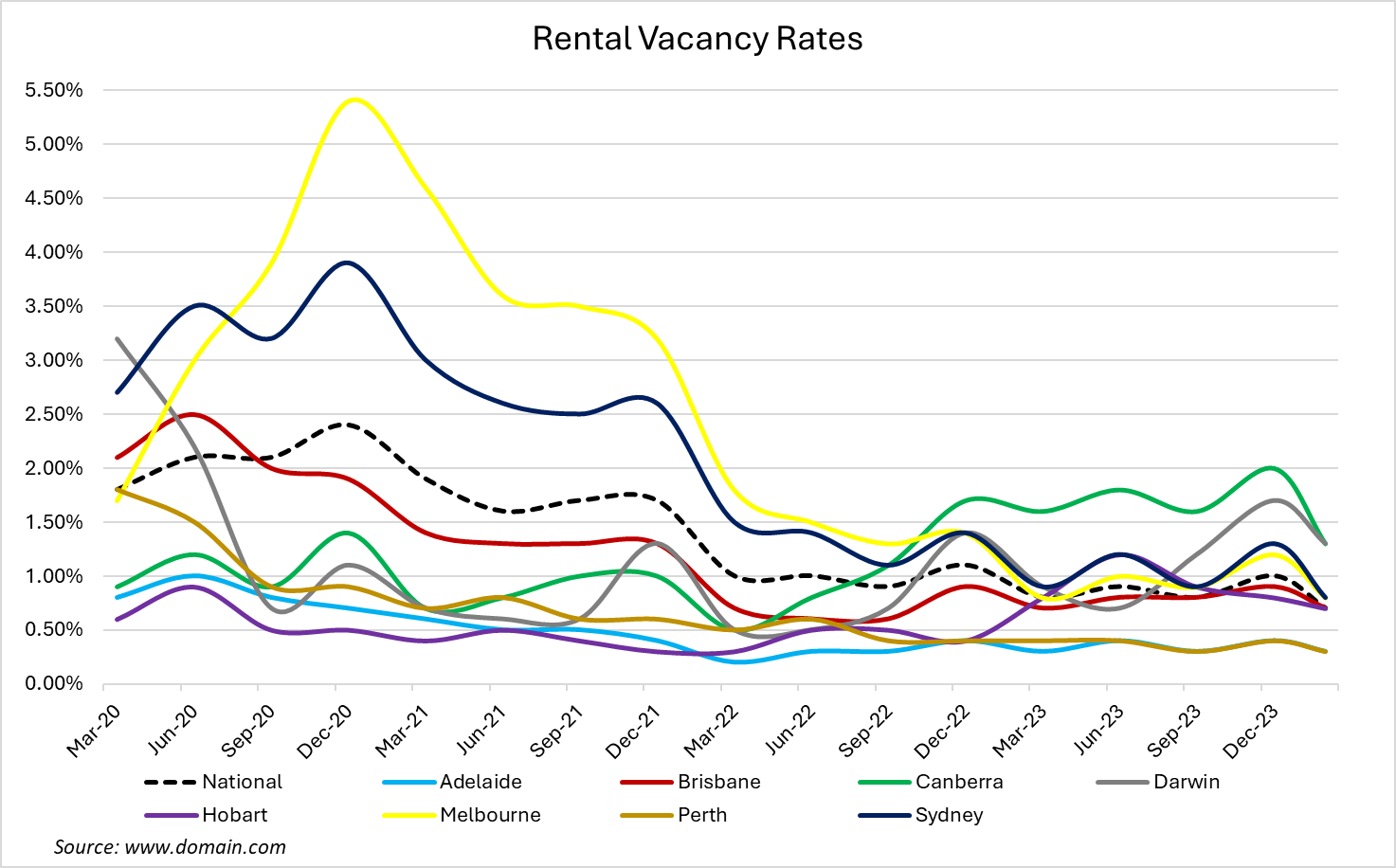

Driven by population growth and an imbalance in supply and demand, the residential property market has tightened to unprecedented levels post COVID19. Rental vacancy rates have plummeted nationally to a mere 0.7%, dipping even lower to 0.3% in Adelaide and Perth (Figure 1), markets which have been particularly affected by the scarcity of dwelling supply and growth in resident populations. For example, Western Australia has seen its resident population grow by 7.0% or ~190,000 between March 2020 and June 2023 - the highest percentage growth amongst all states and territories during the period, while total dwellings in the state only increased by 4.5% or ~50,000 over the same period.

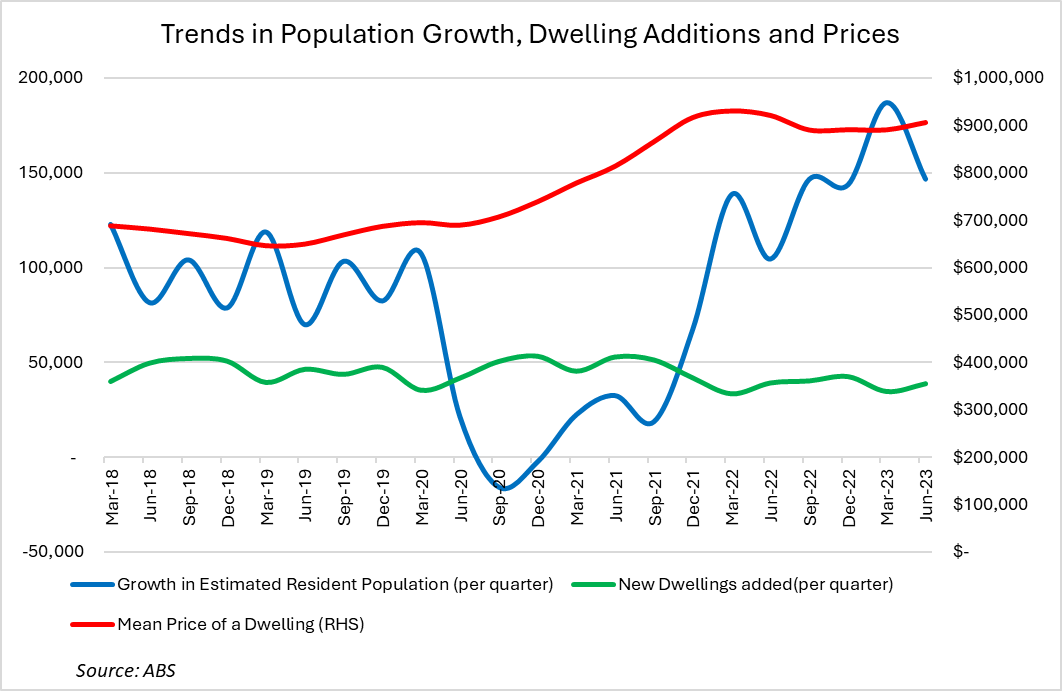

Supply chain issues, labour shortages and other constraints have led to a marginal decline in residential dwelling completions. However, a significant growth in the population from January 2021 onwards has meant that demand for housing has outsripped supply by a fair margin. This is a factor that has been driving unprecedented low rental vacancy rates, rent increases and stable-to-still-increasing property prices across the country (Figure 2), despite the noteworthy increase in interest rates over the past 22 months.

Figure 1

Figure 2

The outlook for residential vacancy rates is to remain extremely low and below historical averages.

Residential dwelling approvals over the 12 month period to February 2024 declined to approximately 163,000 - the lowest level in nearly 11 years1. Net overseas migration is forecast to contract significantly from the 518,000 in FY23 but remain significantly higher than historical averages, at 315,000 for FY242; housing demand is more than likely to exceed supply in the short term. Overall, concerns about future supply continue to linger, particularly in light of dwelling approvals remaining lower than historical averages, higher construction costs and poor buyer sentiment stemming from construction delays and builder insolvencies which present significant challenges for policymakers and the public alike.

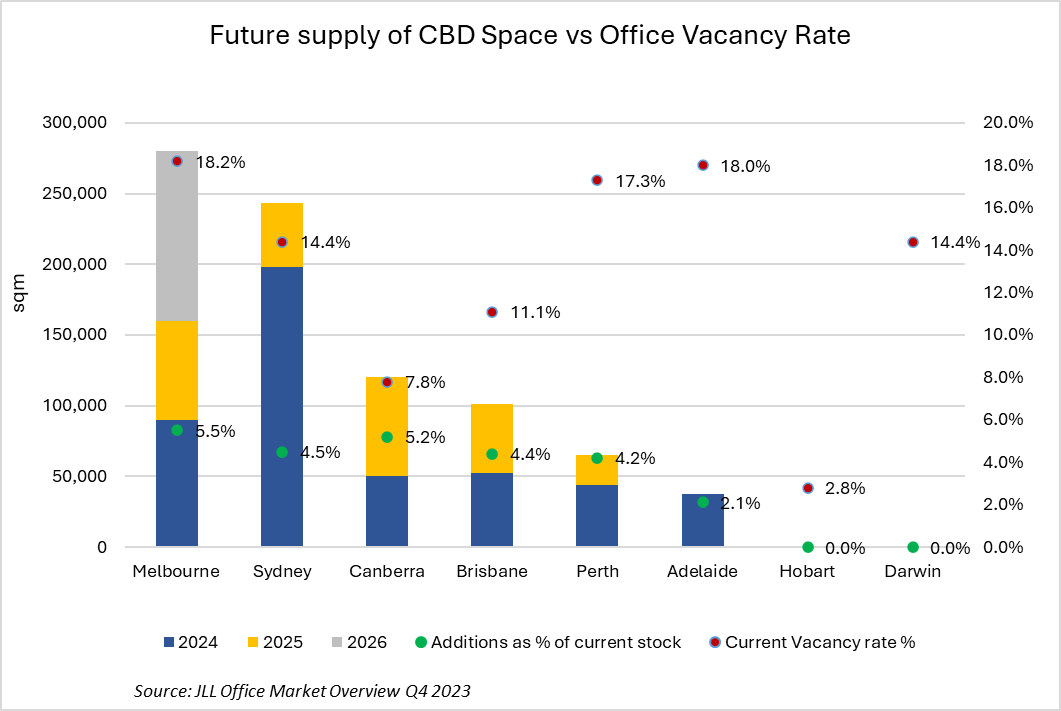

At the same time, the commercial real estate sector has witnessed a surplus of office space as vacancy rates have soared to record highs. The pandemic-induced shift towards remote and hybrid work models prompted many businesses to reassess their footprint, resulting in an excess of supply. Despite reduced demand, previously planned developments continue to arrive through the pipeline, contributing to the existing surplus (Figure 3).

Vacancy rates are at historic highs in Sydney and Melbourne, as well as in smaller markets like Adelaide and Perth. However, the risks they present appear more in the spotlight in the former two, as half a million square metres of new commercial office capacity is scheduled to be added to the pool over the 2024-2026 period. The vacancy rates coinciding with high interest rates are not only signalling a challenging environment for commercial property investors, but a headwind to the work pipeline of commercial builders.

Figure 3

While some might even suggest the simple solution would be to convert vacant office spaces into residential units, numerous hurdles make this an impractical solution. Structural and design differences, along with logistical challenges such as plumbing and HVAC systems, render such conversions impractical and cost-prohibitive. Moreover, even if all vacant office spaces were converted, it would barely make a dent in addressing the housing crisis, given Australia's demand for new residential dwellings.

Meanwhile, discerning tenants for commercial properties are indicating their preference for buildings in prime locations that have sound environmental ratings, good amenities and refreshed fit-outs, incorporating the needs of the modern work environment. While some of these upgrades can be expensive in the short run, they may help in lowering running costs and mitigate the risk that properties not meeting this criteria will lose appeal and remain vacant.

Not surprisingly, prime CBDs of major cities have finite real estate and very few unused land parcels. This, together with recent trends, has driven an increased recognition among commercial property developers and investors of the opportunities presented by refreshing older commercial properties. Refurbishment projects at sites such as 85 Spring Street Office Towers, 1 Dean Street, 121 Flinders Lane & 500 Bourke Street in Melbourne, 8-24 Kippax Street, 55 Market Street & 255 George Street in Sydney, and Gold Tower in Brisbane are just a few examples of projects that have been earmarked or completed recently that have provided an opportunity for commercial builders to capture opportunities in this market.

1 Australian Bureau of Statistics Building Approvals, February 2024

2 Treasury - Opening statement to the Economics Legislation Committee

Related Posts

Highlights:

Mitigate the surge in AI-generated digital forgeries by moving from document-based checks to source-verified payroll data Combat sophisticated salary staging and liar loans with an automated, single source of truth Establish digital trust at the point of contact to protect your organisation from credit and compliance risks.