Credit shopping activity is increasingly concentrated in the high-risk SME segment, while large businesses have scaled back significantly from mid-2023 levels.

The Equifax Market Pulse report, Commercial Spotlight: Credit Shopping in the Commercial Market Q1 2026, reveals several shifts in credit-seeking behaviour of interest to credit managers, risk managers and financial controllers seeking to mitigate exposure in today’s volatile landscape.

These insights highlight how a combination of inflation, the velocity of interest rate policy decisions, and rate variations between lenders is impacting credit shopping behaviour. For context, credit shopping refers to businesses approaching multiple providers within a 30-day window.

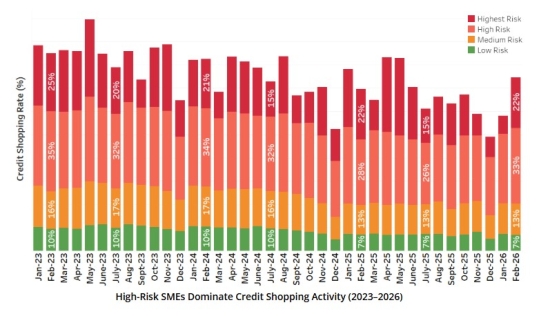

High-risk SME segments demonstrate elevated credit shopping

Equifax data intelligence indicates that while shopping rates for moderate and low-risk business cohorts have remained relatively stable, the high-risk and higher risk segments (with credit scores below 600) have been rising over the last few months and have the greatest share of credit shopping enquiries. After easing to 26% of credit shopping enquiries in mid-2025, one-third (32%) of this segment were credit shopping in Q1 2026.

Overall credit shopping activity is driven by higher-risk SMEs (scores less than 600), with their credit shopping enquiries three times higher in Q1 2026 compared to their lower-risk counterparts with credit scores above 600. This heightened enquiry velocity among sub-prime applicants is often an indicator of liquidity pressure, representing a potential pocket of credit stress that requires close monitoring.

Credit shopping distribution by risk profile

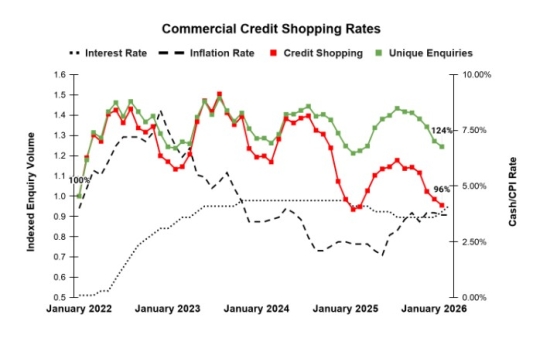

Cost pressures no longer translate into comparison shopping

Interestingly, high demand for capital is no longer driving cross-market comparison shopping. While unique enquiries remain elevated - at 124% of 2022 levels - the urgency to shop around has reduced to the end of last year. Equifax found that shopping rates have dropped to 96% in Q1 2026 due to a lower volatility in interest rates relative to the 2022 baseline.

This widening gap between the need for cash and the willingness to shop highlights a tightening market where competitive deals are harder to find. Rather than submitting multiple applications that could impact credit scores, many commercial borrowers are favouring a single application with a trusted lender.

Stagnant high interest rates and inflation dampen SME appetite for comparison shopping

While both large companies and SMEs maintain a strong appetite for capital (with unique enquiries for both near 125%), their shopping habits have gone in completely different directions. Large business shopping has softened slightly but remains above the 2022 baseline at 104%. Conversely, SME comparison shopping has retracted to 79%, which is 21% below the January 2022 baseline. We envisage this will likely increase over Q2.

With every rate hike in 2023-24, SMEs credit shopping swung widely, but today’s higher-for-longer rate environment seems to have triggered a sense of borrower fatigue. Realising that a long search for a better rate likely won't pay off in the current market, smaller operators are pivoting to one-and-done applications. For these businesses, securing immediate cash flow may have become more important than securing a marginal rate discount.

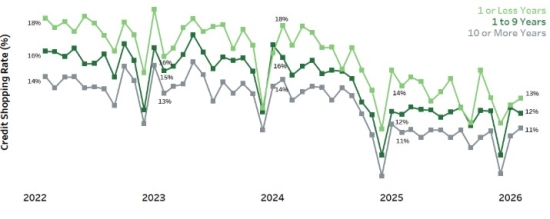

SME credit shopping converges across all business ages

Traditionally, newer businesses (active for a year or less) credit shopped most aggressively, with enquiries hitting 18% in early 2024. While this segment continues to demonstrate the highest tendency to shop, their enquiries dropped by 5% in Q1 2026, closing the gap between startups and established firms.

Mature businesses with over a decade of history generally appear more resilient, with shopping rates dipping only slightly from 14% in Q1 2022 to 11% in Q1 2026. This stability suggests more predictable trading patterns and higher levels of capital and reserves to insulate from macroeconomic shocks. On the flip side, amid geopolitical uncertainty, new business activity has subdued; these newer firms are either accepting the first available approval or are deterred from applying altogether.

SME Credit shopping among all business age segments

Asset finance shopping halves while business loans remain resilient

While business loans have continued to show typical seasonality over the last few years, there was a noticeable pivot across asset finance. Asset finance saw the most dramatic pullback, with credit shopping rates essentially halving since their Q2 2023 peak. Activity has remained relatively subdued since that drop, sitting at less than half of the 2023 levels. This sustained shift suggests that while the government tax write-offs provide a stable baseline, businesses are less inclined to hunt for new best finance deals compared to the 2023 peak.

Business loan shopping has proven much stickier as firms manage ongoing operational costs. The Big 4 banks retain the significant share of business loan enquiries, capturing 25% of all initial enquiries. Equifax intelligence shows that the second enquiry is the real fork in the road; if a borrower makes a second enquiry within the Big 4, they are significantly less likely to look elsewhere.

Navigating escalating risk

While low-risk credit shopping remains stable, the rising volume within the high-risk SME contingent provides an early warning of the mounting financial pressures within the current landscape. To assist credit professionals in defending against escalating credit risk, Equifax offers a range of proactive solutions. This includes our geopolitical conflict analysis report, a monthly service delivering deep-dive research into credit and non-credit datasets to pinpoint which customers across a portfolio are most impacted by macroeconomic shifts and global conflict.

We've also observed a strong uptake in continuous portfolio risk monitoring. A growing number of trade credit managers are leveraging our portfolio pulse check service to move away from past point-in-time assessments. This ongoing visibility allows organisations to navigate current uncertainty and to keep abreast of critical changes as they occur.

Contact Equifax to learn more about portfolio risk monitoring