Shifting Fraud Trends and Growing Exposure

Economic pressures continue to serve as a primary catalyst for financial fraud. The Equifax Fraud Index Report shows a 4% growth in fraud listings over the 2025 calendar year (vs same time in 2024), as rising financial strain heightened consumer vulnerability, making individuals easier targets for scams and money muling.

Fraudsters are narrowing their focus toward high-value targets; for instance, big-ticket credit items like vehicles and commercial assets saw a 112% surge in fraud listings. As bad actors leverage GenAI to produce sophisticated deepfakes and automated document manipulation, we’re seeing a move toward quality, where the high capital involved in these targets represents a critical risk for immediate financial loss.

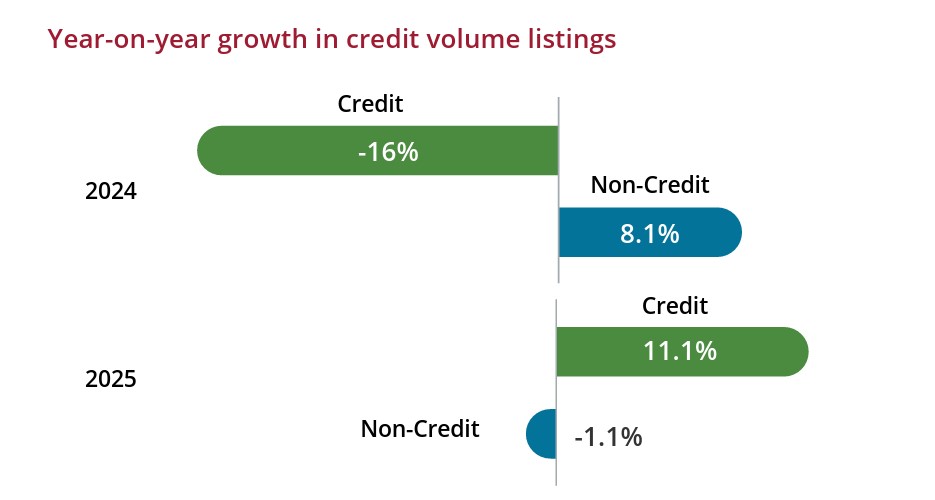

Credit Fraud returns to the Forefront

For the past three years, non-credit products dominated fraud listings. However, 2025 saw a significant shift in this long-term trend, with credit fraud volume listings jumping by 11.1% while non-credit listings experienced a slight contraction of -1.1%.

This shift represents an immediate and direct financial risk. Unlike non-credit fraud, which often involves systemic threats like money laundering, the financial loss from credit fraud is felt instantly - with the risk of unrecovered principal ranging from a $5,000 credit card limit to over $1 million for a mortgage.

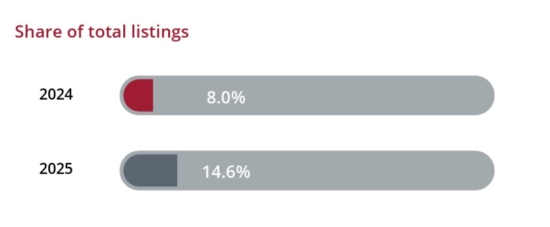

The Explosive Surge in Money Muling

Perhaps the most alarming shift is the dramatic rise in money mule activity. Driven by escalating financial hardship, the volume of money mule listings grew by a massive 90.9%, now accounting for 14.6% of all fraud listings.

Money mules - individuals who transfer illicit funds on behalf of others to obscure their original source - are often recruited via social media under the guise of work-from-home opportunities. While some are aware of their role, others are unwitting participants manipulated by criminal networks. This activity typically targets non-credit products like bank accounts but poses a significant reputational and regulatory risk for any business whose services are paid for with compromised funds.

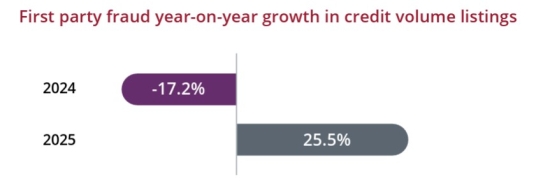

First-party Fraud Accelerates as Identities are Manipulated

We’re seeing a move away from simple identity theft toward sophisticated identity manipulation. While identity takeover remains the largest category, its share of total listings fell to 49.8% in 2025, down from 62.1% in 2024.This is supported by a -16.6% decline in volume listings, suggesting that our collective understanding of fraud is becoming more nuanced and specific. For example, accounts that were previously classified broadly as identity takeover are now being reported as money mule activity.

First-party fraud or ‘loan manipulation’ – where a genuine applicant provides false or conflicting information – is accelerating, with volume listings growing by 25.5%. This type of fraud now accounts for 31.6% of all listings. The use of GenAI has lowered the barrier for individuals to create high-quality falsified payslips and bank statements, often reducing the need for external criminal assistance.

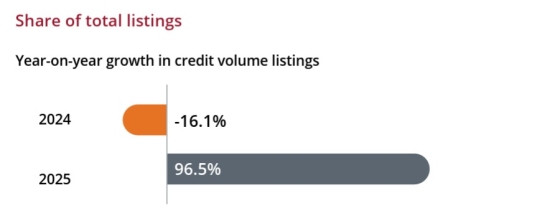

Niche Threats See Aggressive Growth

While still representing a small portion of total listings (1.1%), specialised, high-impact categories like synthetic identities and bust-outs surged by 96.5%. Synthetic identities - profiles created by combining real and stolen data - are notoriously difficult to detect because they can bypass traditional verification and remain dormant for long periods.

Bust-out fraud, where a bad actor obtains credit with no intention of repayment, typically results in multiple missed payments within the first 90 days. These niche threats are being fuelled by deepfake technology and automated document manipulation, signalling a move toward quality and sophistication by bad actors.

Global Spotlight: Canada and Brazil

Equifax operates across diverse international markets to monitor shifting criminal tactics. To provide some insight into this broad view, our Fraud Index Report spotlights recent metrics from Canada and Brazil - regions selected due to their comparable market sizes and fraud environments which offer parallels to the Australian landscape.

In Canada, synthetic identity fraud more than doubled over a two-year period, frequently targeting younger consumers. This trend is mirrored in the mortgage sector, where over 95% of fraudulent Canadian mortgage applications involved the falsification of financial information - a clear parallel to the first-party fraud trends observed locally.

In Brazil, data reveals a rapid escalation in technical methods, with fraud attempts surging by 117.5% in Q1 2025 compared to the previous year. While suspected cases rose by 41.5%, confirmed fraud cases actually fell by 3.4%. This disparity demonstrates the vital importance of real-time anti-fraud technology in preventing loss before it occurs, particularly as scammers increasingly adopt automated, AI-enabled tactics.

Mitigating the Risk

The persistent affordability gap continues to underpin these fraud trends, with Equifax Consumer Market Pulse Q4 2025 data showing a marked increase in financial stress across the board. Late-stage delinquency values have surged for personal loans (10%), BNPL (7.4%), and mortgages (6.8%), while credit card arrears for 18 to 25-year-olds have jumped 28.8% year-on-year.

To mitigate these escalating risks, businesses should adopt a multi-layered approach that secures every customer interaction with less friction. Last year, Equifax processed 97 million searches across its identity and fraud capabilities, helping to prevent over $1.5 billion in attempted fraud and returning that saving to the Australian economy. By leveraging multiple data points, powerful trust signals, and Artificial Intelligence, businesses can better position themselves to identify potential anomalies and protect their interests in an increasingly complex environment.

The data insights in this article are from the Equifax Fraud Index Report 2026, which aggregates data intelligence from the Equifax Identity and Fraud Digital Solutions, enriched with proprietary, public and third-party sources.

Download the full 2026 Fraud Report here.

The content of this document is provided for information purposes only. It does not constitute legal, accounting or other professional financial advice. Further, the information in this document is provided on the basis that all persons accessing it undertake responsibility for assessing the relevance and accuracy of its content. Should you consider it necessary, please seek your own legal, compliance or professional financial advice for application of any this information to your own circumstances.