Equifax Quarterly Consumer Credit Insights: December 2024

-

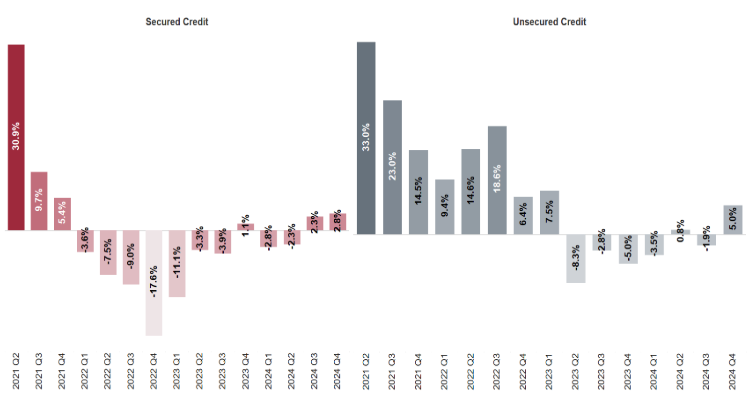

Unsecured consumer credit applications increased (+5.0% vs December quarter 2023)

- Credit card applications grew (+3.4% vs December quarter 2023)

- Personal loan applications increased (+1.7% vs December quarter 2023)

- Buy now pay later applications jumped significantly (+15.7% vs December quarter 2023)

-

Secured consumer credit applications were up (+2.8% vs December quarter 2023)

- Mortgage applications increased (+2.7% vs December quarter 2023)

- Auto loan applications also grew (+3.0% vs December quarter 2023)

SYDNEY – February 2025 – Demand for buy now pay later (BNPL) skyrocketed in Q4 2024, amid an upswing in overall consumer credit demand that indicates growing consumer confidence and an appetite for spending beyond the usual seasonal spending patterns.

Released today by Equifax, the global data, analytics and technology company, the latest Equifax Quarterly Consumer Credit Insights - December 2024 saw consumer demand for BNPL jump +15.7% year-on-year, marking the first growth in demand for this credit type since 2022. Q4 also saw the second consecutive quarter of growth in mortgage demand, supporting a resurgence in consumer confidence ahead of anticipated interest rate cuts.

Kevin James, General Manager Advisory and Solutions, Equifax, said: “While we do expect to see an increase in consumer spending around the festive period, credit demand in Q4 2024 was higher than the previous year, indicating a bump in consumers’ willingness to splash their cash. The increase in credit demand across all categories tells us that many consumers are beginning to feel more confident in the economy and their own financial situations. This is likely to continue, particularly in light of the recently announced decrease in underlying inflation and growing expectation of an interest rate cut.

“Q4 also saw a significant jump in BNPL demand - the first such growth since 2022. This could be partly attributed to sector stabilisation after a period of industry and regulatory change. It could also indicate people moving to BNPL over credit cards for seasonal spending.”

Equifax reports a drop in the proportion of consumer credit accounts in hardship - another indicator of consumer stress relief.

Retail, hospitality workers still doing it tough

Despite the positive indicators, Equifax analysis shows signs of financial stress are prevalent in certain employment sectors, such as retail and hospitality, where younger demographics appear to be relying on unsecured credit to make ends meet.

While national levels saw an overall 5% increase in unsecured credit compared to Q4 2023, demand among consumers working in the retail industry was 28% higher than the same quarter last year. Sitting at over 70% of total applications, unsecured credit enquiries for retail workers are 8% above the national average.

“Retail and hospitality workers, particularly those aged between 18 and 35, are increasingly reliant on unsecured credit. Concerningly, this cohort is also showing higher delinquency rates, which suggests they are not only relying on credit for daily expenses but also falling behind on payments,” Mr James said.

“At the same time, the number of hospitality workers applying for secured credit products like mortgages and auto loans has been falling. So, while we are certainly seeing positive signs among some consumers, there are cohorts that are increasingly being locked out of major financial milestones.”

Demand Change Q4 2024

The Quarterly Insights measure the volume of credit applications for credit cards, personal loans, BNPL, mortgages and auto loans.

Unsecured credit demand, comprising credit cards, personal loans and BNPL grew in the December quarter, up +5.0% year-on-year. BNPL led the way with +15.7% growth, followed by credit cards (+3.4%) and personal loans (+1.7%).

Secured credit demand, derived from mortgages and auto loans, increased +2.8% in Q4 2024 compared to the same period in 2023. Mortgage demand (+2.7%) and auto loans (+3.0%) both increased year-on-year in the December quarter.

IMAGE 1: Consumer Macro Credit Demand – Quarterly YOY

Source: Equifax

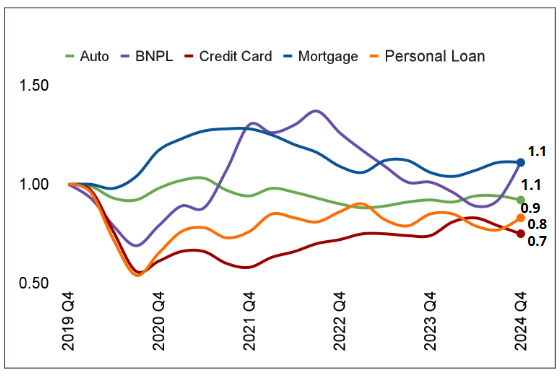

IMAGE 2: Consumer Credit Applications – By Type (Indexed to Q4 2019)^

Source: Equifax

^The data has been re-indexed from 2018 to account for the recent inclusion of Buy Now Pay Later applications:

Re-indexed data to commence in 2018 (previously 2015)

Added buy now pay later and auto loan credit enquiries as a separate trendline (previously rolled up into personal loans)

ABOUT EQUIFAX INC.

At Equifax (NYSE: EFX), we believe knowledge drives progress. As a global data, analytics, and technology company, we play an essential role in the global economy by helping financial institutions, companies, employers, and government agencies make critical decisions with greater confidence. Our unique blend of differentiated data, analytics, and cloud technology drives insights to power decisions to move people forward. Headquartered in Atlanta and supported by nearly 15,000 employees worldwide, Equifax operates or has investments in 24 countries in North America, Central and South America, Europe, and the Asia Pacific region. For more information, visit www.equifax.com.au or follow the company’s news on LinkedIn.

FOR MORE INFORMATION

[email protected]

NOTE TO EDITORS

The Quarterly Consumer Credit Insights by Equifax measures the volume of credit card, personal loan applications, Buy Now Pay Later, mortgages and auto loan applications that go through the Equifax Consumer Credit Bureau by financial services credit providers in Australia. Credit applications represent an intention by consumers to acquire credit and in turn spend; therefore, the index is a lead indicator. This differs to other market measures published by the RBA which measure credit provided by financial institutions (i.e. balances outstanding).

DISCLAIMER

Purpose of Equifax media releases:

The information in this release does not constitute legal, accounting or other professional financial advice. The information may change, and Equifax does not guarantee its currency or accuracy. To the extent permitted by law, Equifax specifically excludes all liability or responsibility for any loss or damage arising out of reliance on information in this release and the data in this report, including any consequential or indirect loss, loss of profit, loss of revenue or loss of business opportunity.

Related Posts

Q2 2026 analysis by Equifax Australia into consumer credit trends highlights how households are navigating ever changing economic conditions.